It is almost fifteen years since I first blogged about growth. My opinions have become more and more uncertain since the earliest “just boost demand already” days. Since then I have contorted in all sorts of ways. Here are some barely connected thoughts.

Having opinions on growth is a little bizarre. The more I have read and thought about GDP, the more uncertain and sceptical I have become. Uncertain, because it is easy to find paradoxes, contradictions, arbitrary judgments of definition; sceptical, because with such a slippery concept it is plain bizarre that anyone normal might have a strong opinion about it. You don’t see GDP, it is numbers in a spreadsheet. So when people profess a strong view about its trend, my first reaction is often “really? How?”. You don’t have an opinion, you just think you have. How can you have a clear view on whether the UK’s potential ability to combine future labour, capital and technology into additional economic product will grow at 1.5% or 2.5% in ten years’ time?

This must sound like a cop-out, or worse: an introduction to yet another of those tedious diatribes about there being more to life than money, growth and GDP. So onto some of the things I find weird.

Shifting relative prices through time There are wildly different trajectories for the productivity of different activities through time. Being a concert pianist, waiter or hairdresser is not much more efficient now than in 1900. The ability to discover information, light a dark room, watch a drama or communicate across a continent has increased exponentially. Shifting relative prices tie these things together, and fix what we see as the actual value of what is produced. So the price index for casting a lumen of light has collapsed exponentially; even since the millennium, some deflator for IT-sector output has been cut by 90%.

I find this marvellous and unsettling at the same time. Depending on how you choose to fix value, you can paint a fantastical and almost entirely useless picture of continuing massive growth. Just value an Internet search at the pre-Internet cost of learning something, or an email at the cost of sending a letter.

Bargaining power is good and bad. A key consequence of these shifting relative prices is how professions that see no persistent tendency to become more productive (say, a high-class lawyer) nevertheless gets to partake in economic growth, the result of productivity gains elsewhere. (see William Baumol’s cost disease). But not everyone does to the same extent, whichis often a reflection of bargaining power. The top lawyer, banker or lobbyist somehow keeps up, the miner or social care worker does not. I am forever tickled by this insight in Ryan Avent’s book about human scarcity (or otherwise): better to be in a low productivity business proximate to high economic demand and with some protective walls around you. The artisanal cheesemaker theory of prosperity.

Lots of innovative/investment effort goes into enhancing bargaining power, not productivity. The branding genius who finds a way to make teenagers love the same mass-produced sneaker for a higher price. The investment in high-rent offices to telegraph prestige to your clients. The first lesson in MBA school is Michael Porter’s Five Forces: fight off the threat from substitutes, new entrants, existing competitors, suppliers, customers. Invest in protective walls so you can keep a profit. It captures the tension that drives the economy forward. But GDP is often higher when the monopolists are winning! Being able to charge a lot more for a product than you put in is value-added. In contrast, really successful innovation can have a first-order effect of lowering GDP. If an activity such as maintaining a bank’s leger once needed 1000 sweating clerks, and now requires a simple software programme, the effect might be a smaller direct GDP footprint.

Market size matters for potential GDP, do we discuss it enough? The gap between US and UK productivity is longstanding and much commented upon. There are plenty of reasons for it. The most convincing I know is the size of the US market, which brings home a really important factor for productivity – operational gearing. Finding a bigger market for the same fixed asset base is the simplest way to get more bang for your buck. Hence also the magic of export-led growth, and one of countless reasons to be pro free-trade. I think this is under-emphasised in the “People, Capital, Ideas” schema that Sunak pushed, a good expression of the orthodoxy.

Productivity growth was more reliably strong when manufacturing was pre-eminent. At first this feels odd. Physical activities have real resource limits that you don’t see in more intangible services. It takes ten times more steel to make ten cars than one. Assisting in the sale of 10 houses should not take ten times as many estate agents. But the highpoint of (Western) growth coincided with the highpoint of manufacturing, and I can think of good reasons why. Physical processes are amenable to constant improvement. Innovations like electricity, computerisation, containerisation, the assembly line, just-in-inventory management all have a long way to go. Tradable goods are very hard to hide from competition, the great driving force. So there is reason to think that the grand shift from manufacturing being 30% of the economy to 10% (and future 5%) must have consequences.

Hence a nagging feeling that the shift to a more intangible economy is not good for GDP growth. The excellent book of Westlake and Haskell deserves a much fuller appraisal than this one point. My hazy concern: intangible investment is less spillover-rich and therefore less growth-rich than one might imagine. It isn’t all inventing Google (which obviously the authors explain). Often it is about company’s own private productivity enhancements, or reputation or brand, and I don’t see it spreading all over the economy like, say, a new invention. On the input side, I can easily picture intangible capital as a fast-depreciating asset. Consider the trillions that the the financial sector must spend software just to keep the wheels turning. It is also subject to cost disease – intangible investment is human-heavy. All unquantified thoughts, but they mean I see no contradiction between “growth in productivity may be slowing” and “we are heading into a more and more intangible economy”.

Another wrinkle that bugs me: how should we think about the concept of (what I call) fake GDP? What is the right approach to value, for example, all the incomes that were generated in the ecosystem around a busted cryptocurrency? It now turns out it was just a few thousand fools throwing real or fake money at one another, consulting, meeting, emailing, writing software, and now it is all bust. Was it real GDP at the time, and now not? Never real in the first place?

I wonder how much of the economic activity that led up to 2007-8 should be revisited as “not actually GDP”, and whether our growth trends before 2007 were not sustainable – but how? It wasn’t shown through inflation …

And what about demand? For about 10 years I felt that the slow pace of demand growth had caused low productivity. See the point about operational gearing: underemployed resources are less productive. Now we are seeing an inflationary episode, does that mean I was wrong? Or should we be MORE optimistic now, knowing that every productivity gain will free up labour resources that the economy is more likely to need?

GDP/consumer surplus is not as fungible as being a single figure in a spreadsheet implies. Think about the challenge of elderly care. Care homes are incredibly expensive: property costs plus labour costs in a risky environment. I may once have felt good about the prospects for technology to improve this radically: the aged relative surrounded by iPads, remote delivery of services, constant connection. Now I’m aware of how irreplaceable are the services of younger people. Technological advance in one part of the economy doesn’t just translate into higher welfare in another part. Cheaper video streaming doesn’t solve loneliness or the need for physical nursing. What you need is a political means by which the surplus production is transferred from advancing to stagnant sectors.

Any longer-term growth pessimism I have, in summary, is fuelled by concern about how a more services-heavy, aged, environmentally-challenged world can use innovation to address its problems, when innovation is often geared towards #rent-seeking, the provision of low- or zero-marginal goods, meaningless growth in consumer surplus, and not the really hard constraints in energy, the environment and human services. But since the UK is not at the frontier, this is only partially relevant – we can surely do better. And I have a very crude thought on prospects for that, to which I now turn.

So what can public policy do? Escaping the average is hard

A friend told me that a prominent former Cabinet minister read my blog about why you can’t just “unleash growth” and liked it. It made me think, however, about how I would respond if this statesman asked me for actual positive ideas, and whether I am just in the “too hard” camp. Well, this is what I think:

- There are good ideas that can increase potential GDP. Every government should be trying to promote them, and fight the opposite sort. If you want a representative list of the sort of buffet from which future Growth Ministers might graze, take this lovely blog* post from Tom Westgarth and Andrew Bennett (hat tip, Stian Westlake)

- If (straw man?) anyone is suggesting such a list can get us to 2.5/3.0% growth then my questions would be about baseline and about scale.

In terms of scale, I made this point in the earlier blog, and will again in a business investment piece. Do not underestimate the vast stock of what is already there, and the relatively small flow of what you are adding. If you increase government investment by a massive £20bn, that is still very small compared to the £4.6trn of existing UK capital. If you do something truly wondrous about skills, remember that there are 30m+ workers, most of them out of the education system. It is an oil-tanker.

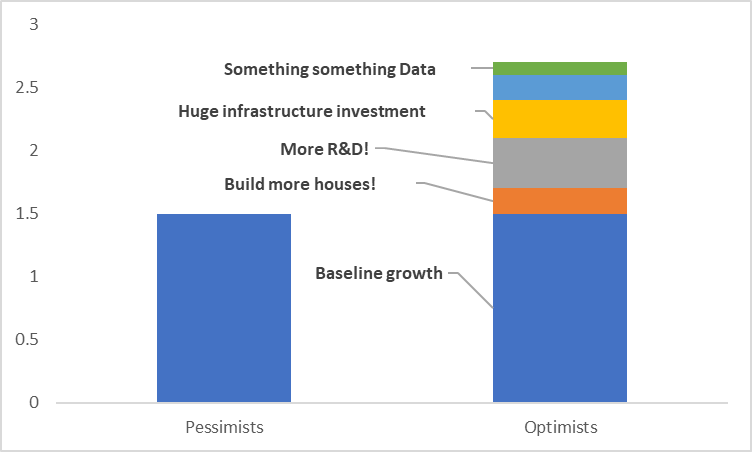

In terms of baseline, let me try to put it figuratively. Suppose the pessimistic view is the OBR’s – that we are heading for 1.5% annual GDP/head growth. And then the optimist comes along with his growth-boosty things. This is how I imagine an optimist seeing it:

“You thought growth was stuck at 1.5 – but what if we carried through my good ideas of building more houses, boosting R&D and something or other with data? NOW what do you think?”.

And my response is: don’t you think any good ideas were in the baseline that got us to 1.5? 1.5 is a pretty good growth rate by historical standards, and will have included a lot of policy improvement. It is a lot higher than we have recently enjoyed, despite this being the era of the Smartphone and the Internet – two wondrous general purpose technologies. Do we know what the OBR assumes the government will do for the next 20 years – is it assuming no good policy whatsoever? Maybe it doesn’t have all your ideas (maybe they aren’t all good) – but maybe a lot of other ones.

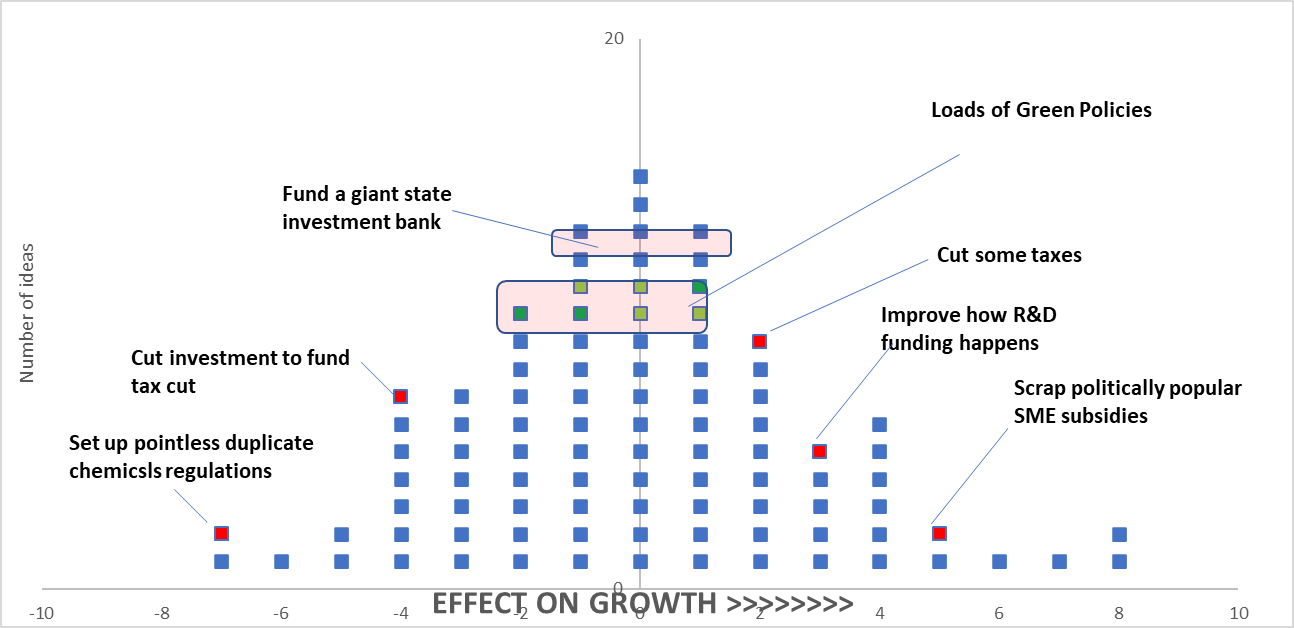

Keeping it figurative, this is how I instead picture the job of the embattled, pro-growth policymaker in government, thinking about the ideas coming along:

Even this is idealistic. The ideas do not sit independently (so you cut taxes, but have to cut investment too, making it a wash). And they are not neat dots, but smeary puddles. Your idea to create a giant investment bank? It might help things, it could badly mess them up!

The point I am laboriously making: you think it is a game of pushing two or three big Pro Growth policies, and maybe fending off a few bad ones? I wish! Politics isn’t pro- or anti-growth, that is way too simple (though read Duncan on this). Politics is above all hectically busy. It is busy doing hundreds of things that are pro- or anti-growth, and you need a tireless machine to be fighting the bad ones, pushing the good ones (this is why you need the Treasury. They stop bad stuff!) But there are many, many bad ideas, and your good ones each require effort. On average, if you left the politicians alone, they will do bad things. And so, in the end, like any game of multiple dice throws, you need to be very lucky to do much more than hit the middle of the bell curve.

The average. It is a tyranny.

*I am not endorsing all of these blog ideas. They feel like they are scattered across my bell curve, entirely uncosted (as the authors acknowledge) and in many cases require the kind of statist intervention that just isn’t executed well. Am particularly amazed at the call to plonk so much mass transit everywhere. But it is a good buffett

One thought on “Umpteen reasons I am so uncertain about growth ”