For someone who spends as long as I do noodling over the UK economy, it is flat out embarrassing that I do not have an immediate and confident answer to this question.

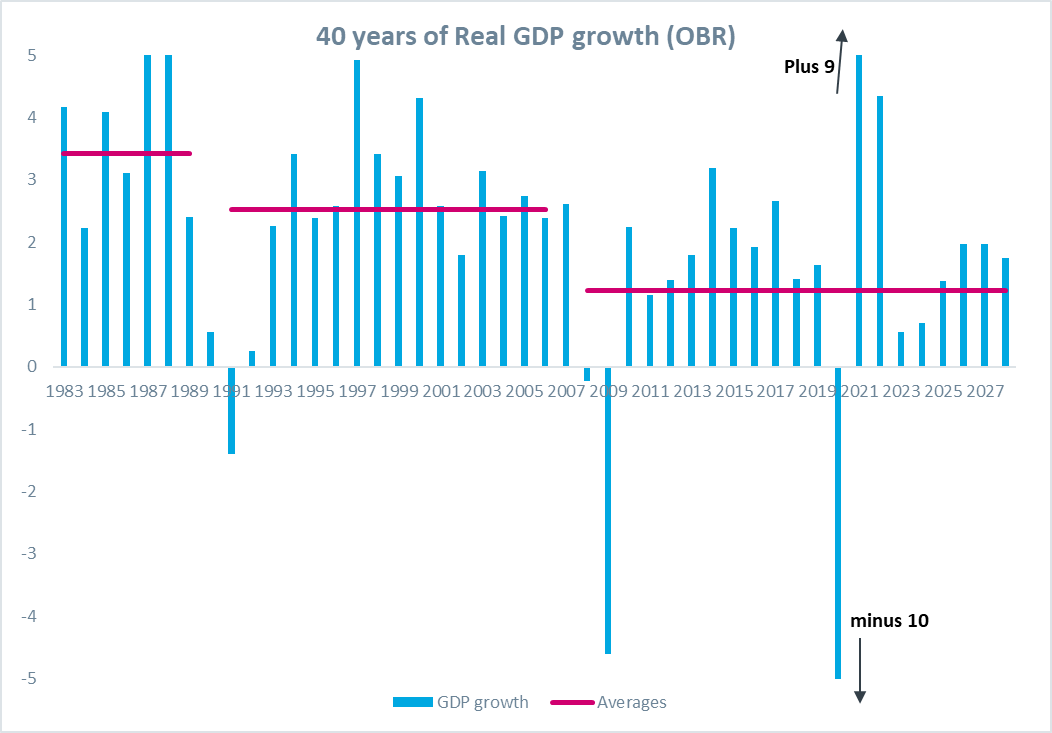

Here is a reasonable contender for the most important chart of the era.

Taken from OBR figures (so easy to do), this shows successive key eras of RGDP growth: the last 7 years of Thatcher, the long Goldilocks recovery under Major and Blair, and then the years of the four crises: Financial, Brexit, Covid and Ukraine – including projections. In each new era, the average growth rate has fallen down a step: 3.4% per annum in the first, 2.5% in the second, 1.22% in the last. I have snipped off the axes to prevent the ridiculous Covid years ruining the appearance of the chart.

Why has this happened? It is easier to dismiss the bad or lazy takes than provide a really strong positive answer. For example, it is not a matter of “being in all the wrong sectors”, or bad industrial policy as some would characterise it: we are not that different from the USA or other growth champions (I tried to take on this thesis and much more in a 2021 piece here). Fantasize all you like about what might have happened had we not allowed manufacturing to wither somewhat, but when a sector is 10-15% of the economy, it simply cannot explain a fall in the whole of it to that degree. Had we continued to grow at 2.2% since the financial crisis, by 2019 we would have had an economy £240bn larger: that is more than the entire manufacturing sector.

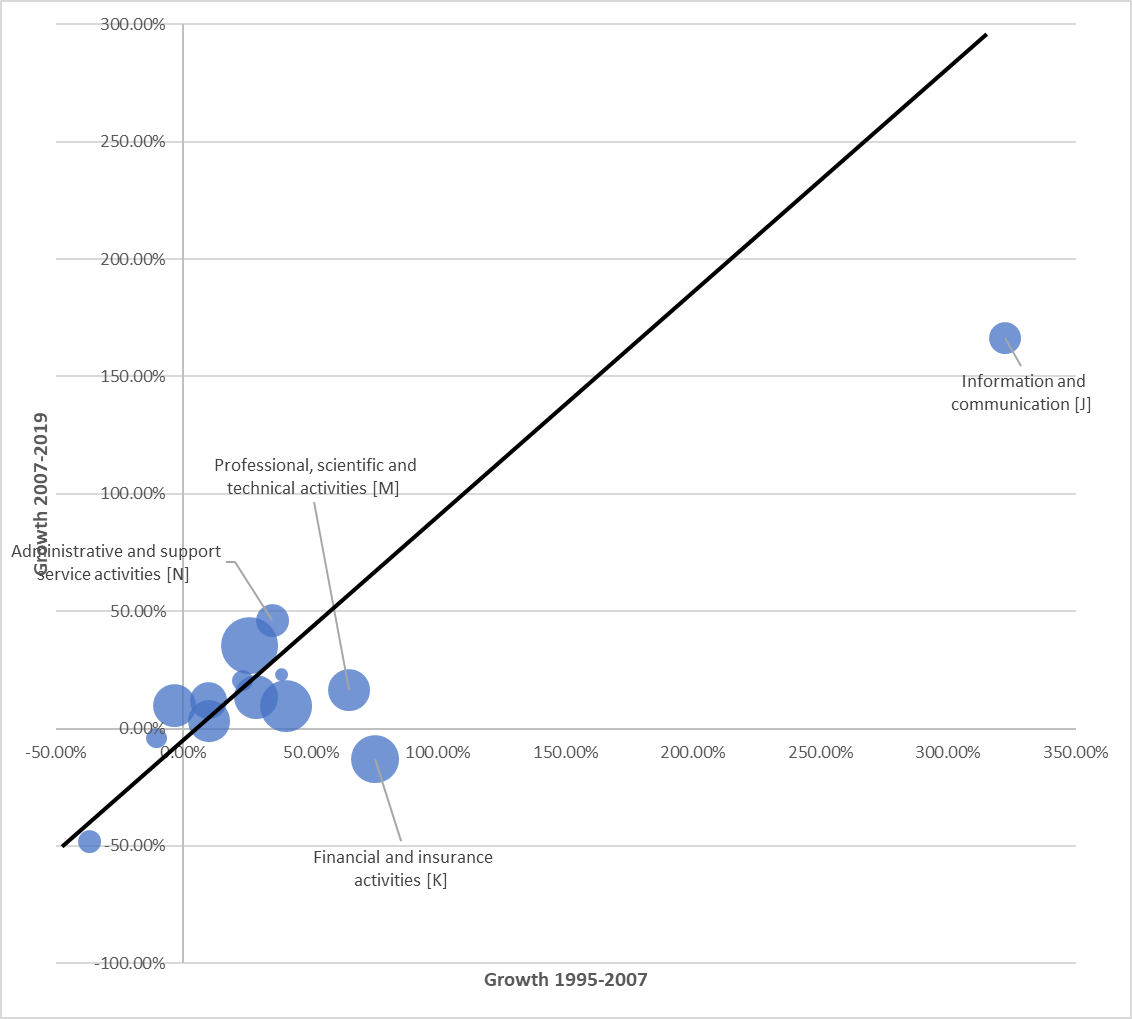

It is more feasible to look at the failure of the big services that provided a lot of pre-crisis growth: IT/comms, Financial services, Professional services all failed to grow since the GFC like they did in Goldilocks, with IT a particular failure. We maybe fail to appreciate how extraordinary the dozen years up to 2007 were; we should also be alert to the difficulty of properly capturing the value of services like the Internet suddenly arriving. And we can all appreciate how the Financial Sector could not easily have replicated the 75% real terms growth that happened in those miracle years.

What are the other theories? Some admirable folk are obsessed with our low building rates, but the charts they publish tend to show the problem started way before the big growth slowdown (as far as I can see, the last birth cohort to head into its late twenties not needing to spend 20% of its income on housing costs was the one born in the mid 1960s. That is at least how I see this chart)

And I do not think you can easily make the housing sector responsible for the failure of the whole: I tried to do the numbers once here.

Can you blame slowing technology? Perhaps, though you need to dig deeper. These charts of mine suggest that improvements in certain key, big consumption items may have just run out in the last 10 years – clothing, automobiles, big appliances – and the things that kept improving somewhat (online digital things, say) are just not that important to the consumption basket. Add in the sharp increase in energy prices recorded to the last year, and Baumol’s Cost Disease wearing away while our need for services rises relentlessly, and slowing graph, decade by decade, is almost inevitable. But it does little to explain why the UK is perpetually behind other countries with much the same access to finance and technology as we have, in terms of labour productivity. Nor is it easily a story of poor educational outcomes.

So what DO I think? Obviously a mishmash of everything, but with a particular emphasis on structural inevitabilities, bad luck and some bad government.

In the last 15 years we have been hit by three crises that might be once-a-generation (the financial crisis, Covid and the Ukraine price shock), while managing a historically large governance blunder (Brexit, and the governing uncertainty that came with it), all at a time when structural headwinds are against us (an ageing society, the end to some of the easier wins from globalisation, and the energy transition). We have, in my opinion, been ruled by governments mostly with the wrong mindset: too lazily laissez faire on industrial strategy, and for a few years a little blithe about the risk of weak demand, though I don’t think these two failings account for more than two or three ppts of lost opportunity. The year 2007-8 marks an unusually difficult high point to match, because financial sector output was unsustainable in some way, the UK particularly exposed to it, through other services too.

But we are fundamentally still a good capitalist economy with trusted institutions, stable rule of law, financial markets that broadly work, quite well educated people and an underlying openness to the world in spite of some of our worst politicians. We ought to be able to do better in the years ahead than people fear, or perhaps than the OBR projects. It doesn’t need a “plan” for growth, any more than the 60 years after the War needed one: approximately free markets are always trying to seek out new demands, new techniques, new uses of capital and so on.

So I am pretty optimistic, particularly if we see an improvement in the quality of political leadership over the next five years. On average, it ought to be better than the last five.

One thought on “What is your favourite explanation for our fall in growth?”